2015 Indiana Consulting Foresters Stumpage Timber Price Report

This stumpage report is provided annually and should be used in association with the Indiana Forest Products Price Report and Trend Analysis.

Stumpage prices were obtained via a survey to all known professional consulting foresters operating in Indiana. Reported prices are for sealed bid timber sales only (not negotiated sales) between a motivated timber seller and a licensed Indiana timber buyer. The data represents approximately 10 to 15 percent of the total volume of stumpage purchased during the periods from April 16, 2014 through April 15, 2015. This report has been published since 2001.

The results of this stumpage price survey are not meant as a guarantee that amounts offered for your timber will reflect the range in prices reported in this survey. The results simply provide an additional source of information to gauge market conditions.

WHAT ARE SEALED BID TIMBER SALES: The sealed bid timber sale process is for trees marked by a professional forester. The species, number of trees and volume in a sealed bid sale are determined prior to the notice of sale. A notice is sent to licensed timber buyers who then inspect the timber and offer a price for said trees at a predetermined time and place. Under conditions determined in the bid notice, the owner then accepts or rejects the bids.

Upon acceptance of the bids by the owner and the fee paid, the owner then conveys the right to cut the advertised trees to the purchaser. This is frequently referred to as a lump sum timber sale. More detailed information on this process is available in Purdue publication FNR 111 – “Marketing Timber” or FNR 138 – “How to get the Most from Your Timber Sale”. These publications and others are available on line at: http://www.agcom.purdue.edu/agcom/Pubs/fnr.htm

This report reflects “spot market” prices, not necessarily the average price paid by timber buyers. The bidding process used by consultants “spots” the maximum amount any buyer is willing to pay for a particular lot of timber at a particular time and place, not the average price paid for timber. High bids frequently reflect an urgent need for timber because of special orders for lumber or veneer, low log inventories at the buyer’s mill, poor logging conditions due to wet weather, or other special conditions.

One service that the consulting foresters provide is knowledge of the timber markets for specific species and grades / quality. The consultant forester may advise the landowner to adjust the species and quality of a harvest at a specific time due to current demand. For example the black cherry markets have been soft for several years therefore the advice may be to hold onto that growing stock until the markets improve provided the tree is in good condition. Because of the strong black walnut or hickory markets in 2014 the advice may be to select a few more for harvest.

Hardwood lumber is sold in a highly competitive commodity market. Competition comes from mills within the state, region, and hardwood lumber producers in the Lake States, Northeast, South and Southeastern production areas. This market competition means that the cost of stumpage in other producing regions determines in part the amount Indiana mill and loggers can pay for stumpage. If all timber were sold on a bid basis the spot market would no longer exist and the average of the highest bid price offered would be lower than now observed. This explanation isn’t meant to deter you from seeking the best available price. It’s meant to explain the apparent discrepancy between the two price reporting systems.

CATAGORIES OF TIMBER REPORTED: The prices reported are broken into three sale types; high quality, average quality, and low quality. A high quality sale is one where more than 50 percent of the volume is # 2 grade or better red oak, white oak, sugar maple, black cherry, or black walnut. The low quality sale has more than 70 percent of the volume in # 3 “pallet” grade or is cottonwood, beech, elm, sycamore, hackberry, pin oak, aspen, black gum, black locust, honey locust, catalpa, or sweet gum. The average sale is a sale that is not a low quality sale or a high quality sale as defined above.

In the 2008 report some minor adjustments were made in the categories from previous surveys. White ash was previously included as a component of the high quality timber sales and hickory was previously in the low quality group. No additional changes in the groups have been made since, so the 2015 data should compare well with data collected from 2008 thru 2014.

SALE ACTIVITY CONTINUES TO INCREASE: In 2015 there were 368 sales (plus 12 negotiated sales) up from 330 sales (plus 14 negotiated sales) in 2014 and 289 sales and 290 sales (plus 13 negotiated sales) in 2013 and 2012, respectively (Table 1).

Eighteen consulting firms reported data in 2015, the same number as in 2014. From 2009-13, 16 to 21 firms reported data in a given year. Fourteen firms that have reported since 2011 showed an increase in the number of sales from 277 (2013) to 318 (2014) to 351 sales (2015) during the last 3-year period. All consultants that reported had sales in this reporting period.

Table 1. Number of sales by quality types during the 2012-15 reporting periods.

Reporting Low Medium High Total

Period Quality Quality Quality

2015 38 208 122 368

2014 52 178 100 330

2013 43 167 80 289

2012 32 157 101 290

The increase in the number of sales the last two years is due to the strong timber markets and an increase in landowner awareness of forest health concerns, particularly emerald ash borers.

BIDDING STAYS CONSISTENT: In 2015, a total of 1,702 bids were received on the 368 sales for an average of 4.625 bids per sale which is nearly identical to the 4.62 bids per sale in 2014. This average per sale includes 5.82 for high quality (5.85 in 2014), 4.24 for medium quality (4.43 in 2014), and 2.89 for low quality (2.89 in 2014). The 13 year averages are 6.02, 4.56, and 3.14 bids per sale for the respective quality groups.

The reduction in bids the last couple years is likely due to an increase in the volume on the market and a higher number of lower and medium quality sales that typically draw less interest. The decline in the 13 year average is due to a decline in the number of sawmills and producers that were unable to survive the recent recession.

SALES VOLUME INCREASES: The total stumpage volume 36,773,866 board feet plus 683,235 bd.ft. negotiated is up considerably from 28,931,192 board feet (plus 1,323,866 bd.ft. negotiated) sold during the 2014 period, 2013 - 28,650,085 bd. ft., 2012 - 25,164,871 bd. ft., and 2011 - 24,367,251 bd. ft. This is up considerably from the volumes reported during bottom of the recession 17,687,648 bd. ft. in 2010 and 19,256,439 bd. ft. in 2009. The volume of timber reported is also up from the volume of around 25 million board feet sold in 2008 and 2006 (pre-recession).

The volume of high quality sales totaled 11,681,259 board feet which was higher than the 10 million board foot level reported before the recession in 2008. From 2011 thru 2014 the volume was between 8,583,450 board feet and 8,725,647 board feet.

Medium quality sales totaled 22,606,525 board feet up considerably from the 17,690,376 board feet reported in 2014. The volume of medium quality sales has been gradually increasing with a good part of that increase due to shifting the ash from the high quality to the average quality category and the hickory from the low quality category up to the medium quality category. The amount of ash on the market has also increased due to the spread of the emerald ash borers.

Lower quality sales dropped slightly with 2,486,082 compared to 2,657,366 board feet in 2014 and from the 2013 levels of 3,113,243 bd. ft. The volume included in the lower quality sales has generally been around 3 million feet including negotiated sales although it was lower during the recession.

VALUE INCREASES: Total timber value sold in the 2015 reporting period was $19,207,898 which is up considerably from $12,363,424 in 2014 period as well as the previous several years (2013 - $10,494,377; 2012 - $10,559,277; and 2011 - $10,678,849). Value sold in 2010 and 2009 ($6,889,190 and $7,278,302, respectively) were much lower. Total value by type was $8,760,973 for high quality (up 69.9% from 2014 but had been reasonably stable since 2011); $9,726,133 for medium quality sales (up 50.0% from the 2014 period and has gradually increased since 2011; and $720,792 for low quality sales (up 15.2%).

RECORD STUMPAGE PRICES: The average stumpage price for this period for the each category was the highest or close to the highest that we recorded in 2004. High quality was $750/MBF ($651/MBF in 2004), average quality was $430/MBF ($433/MBF in 2004), and was low quality $290/MBF ($266/MBF in 2004). The average for all sales was the highest recorded at $522/MBF ($506/MBF in 2004) and up considerable from 2014 - $427/MBF.

One exceptionally high sale this year selling for $6.66/ board foot significantly affected the overall stumpage prices. The effect of that sale increased the average stumpage price for the High quality sales from $729/MBF to $750/MBF and the average stumpage price for all sales from $515/MBF to $522/MBF. The median stumpage prices for the high quality sales remained the same ($733/MBF). Even without this sale, prices in 2014 were considerably higher than the record prices reported in 2004.

This year there were 36 sales (9.8%) that brought over $1.00 per board foot up considerably from 13 sales (3.9%) in the 2014 report, and the 3 sales (1%), the 16 sales (5.5%), and the 19 sales (7.0%) in 2013, 2012, and 2011 reports, respectively.

Landowners should keep in mind that markets are only one consideration. One of the most important factors on when to sell a specific tree is the condition of the tree (is the tree increasing in value or declining – is its condition (health and vigor) going to improve, decline, or stay the same) and what impact will that tree have on the future stand (is it competing with a better future crop tree or will it be a benefit or negatively impact natural regeneration).

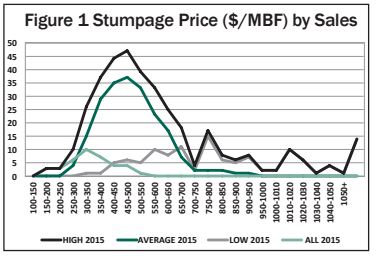

STUMPAGE PRICES: Figure 1 shows the stumpage prices for all sales, high quality sales, average quality sales, and low quality sales held from April 16, 2014 thru April 15, 2015. The data shows a nice bell curve for low quality, average quality and all sales. High quality sales generally have a wide range of stumpage prices due to higher quality timber or potential veneer therefore the stumpage price fluctuates considerably. All sales, low, average and high quality can be affected by sales with a potential veneer component. It is important for landowners to realize their timber typically will fall within the range of stumpage prices, but probably will not fall into the outlying values. This makes it important to work with a professional when selling timber so that you know what you have. For example, a few walnut trees can greatly distort the value of a low quality improvement sale, dominated by pallet material.

High Quality Sales: The average stumpage price of high quality sales was $750 per 1000 board feet (MBF) up considerably from the stumpage price of $591 MBF in 2014 and higher than the highest price reported in 2004 ($651/MBF). The median stumpage price this year of $733/MBF which is considerably higher than the previous high reported in 2004 of $610/MBF.

Average Quality Sales: The average stumpage price for average quality sales was $430/MBF up significantly from $377 from 2014 $338/MBF in 2013 and nearly as high as the peak level in 2004 ($433/MBF). The median price was $431/MBF also up from $354/MBF last year but considerably lower than the peak of $510/MBF in 2004. The large variation in the median value $510/MBF and the mean or average value $433/MBF in 2004 is a concern, unfortunately these numbers predate my data collection and are not available. This is the highest level since 2004 and the second highest reported.

Low Quality Sales: The average stumpage price for the low quality sales was $290/MBF which is the highest reported. The previous high reported was in 2004 - $266/MBF. The median price was $288/MBF which is very close to the previous high from 2004 of $290/MBF.

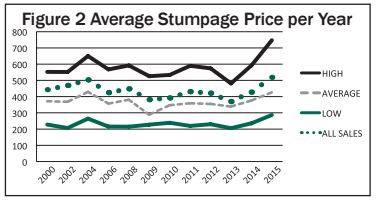

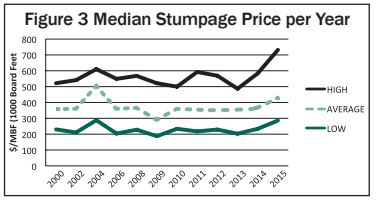

The weighted average stumpage price by sale type (obtained from this survey in 2000, 2002, 2004, 2006, 2008, 2009, 2010, 2011, 2012, 2013, 2014) is reported in Figure 2. The weighted average of the stumpage price is the total value ($) for each sales group (high, average, low) divided by the total volume by sales group. The median stumpage price by sale type per year is reported in Figure 3. The median price is the amount where half of the sales are higher and half are lower. The price reported is per 1000 board feet (MBF) of standing timber. To obtain a price per board foot, divide the price by 1000. An average price of $522 per thousand (MBF) is the same as 52.2 cents per board foot stumpage. Below is a statistical summary for all three sale types.

SUMMARY:

Timber Markets: This year’s data indicates that overall markets are very positive. Prices for many species have returned to the levels prior to the recession and even surpassing the highest level reported in 2004. This has resulted in more timber going on the market which may in turn lead to an oversupply and a decrease in the price. The larger trees and better quality timber, as usual, have the most demand and are generally in the least supply, and therefore, they have the highest price. Demand for some species, such as black walnut and white oak, was extremely strong; hickory and sugar – hard maple was strong. Red oak was in more demand and the prices improved but are still volatile. Good “white” soft maple continues to do well. Even though emerald ash borers continued to spread across the state with mortality visible in most areas, demand and prices were strong, especially if the trees were still alive. Black cherry markets are still down from historical highs. Pallet markets were especially strong in some areas of the state.

World Market: Fortunately much of the timber from Indiana is high quality and in demand throughout the world and Indiana’s forest industry has positioned itself well to compete in the global marketplace.

Lower Quality Sales: Demand for low quality timber has been very strong this year, particularly if the timber is near a pallet mill or if good access is provided. It is important to remember that low quality sales are generally improvement cuts where trees are harvested that are impeding the growth of future higher value crop trees, therefore the opportunity costs of leaving the trees may cost more in lost productivity, so it often is not advantageous to delay selling lower quality if the price is reasonable.

Larger Inventories and Equipment Upgrades: More stability with the economy shows industry carrying a larger stumpage and log inventories than they had the last few years, although it is still not as large as the inventory prior to the recession. With the strong market most logging jobs are still being cut fairly rapidly although the poor weather conditions have caused delays. Trucking has been especially difficult with the weather. There appear to be more equipment upgrades in the field with more grapple skidders and whole tree harvesting machines. This should increase the productivity of the logging crews. There continues to be a shortage of new loggers.

Forest Health Concerns: In today’s global economy we continue to be impacted by new, often exotic pathogens that threaten the forests. Emerald ash borers, Asian long horned beetle, and thousand canker disease are potential threats that could or are causing significant problems. It is important to be aware of threats but understand that these threats may or may not be imminent. Forest health issues make professional advice even more important to get an unbiased update on the current status of each threat as it relates to your property.

The comment section below is offered to our readers by the consulting foresters who participated in this survey:

Black walnut markets were extremely good thru the winter but appear to have dropped this spring. Optimistic they will return as strong this fall. Walnut was in high demand over the winter months and the spring of 2015, but Walnut lumber demand has softened. Big walnut and big walnut veneer is still prized.

Ash markets are strong even though they continue to be impacted by the spread of emerald ash borers throughout the state. The markets depend on how long trees have been infested and the size and the quality of the trees. The value tends to drop drastically when the bark sloughs from the tree. Just now seeing infestation for first time so we are selling ash due to impending EAB infestation down our way (southern Indiana). Poplar and ash are easy to move, mills want them.

White oak demand still strong, especially for quality or larger quarter sawn logs. Big White oak is highly sought after and is generally easy to sell. There are several good markets for the whole tree. There is still a good demand for stave white oak.

Sugar / Hard Maple the market for sugar maple is good if clean and in areas that tend to produce white wood. Sugar maple has been weakening some but the rotary market is good.

Soft maple continues to move well, especially if white.

Black cherry markets are still not where they were. Cherry markets may never return to as high of level because of innovations and substitutions by industry to mimic Cherry wood with stained soft maple and exotic hardwoods.

Red oak has is still volatile, moving very well at times then slowly. Markets for larger trees and quality have been more stable. Red oak markets are softening, and especially, Black oak

Tulip (poplar) Poplar (tulip) and ash are easy to move, mills want them, especially the larger sizes.

Hickory markets are good, especially if large clean trees but demand has weakened some. Flooring markets are currently oversupplied.

Low grade / Pallet demand was very strong, especially if close to the mill. The price has leveled off, even declined somewhat but still very high. It is still an excellent time to move your lower quality timber in many areas of the state.

Pine is easy to sell in most instances (south). It goes into pallet and a lot is being chipped. There are a few niche markets for grade pine. I have found that certification is beneficial where the pine is suitable for chipping.

GENERAL MARKET COMMENTS:

• Overall we had a very good sales year, but our opinion is that it may be time to back off on timber sales for a few months except dying ash, due to a glut of hardwood lumber and logs at the sawmills. I’ve heard from buyers who agree and disagree with that opinion, but the market report seems to indicate a downward price trend for the last three months leading into the summer on all species except ash and tulip.

• The standing timber prices are staying strong especially if the sales contain white oak, good ash and poplar in them. Just recently, the red oak and sugar maple lumber markets have almost crashed. Everyone I talk to is finding it hard to sell red oak, black oak and sugar maple logs and I think the sawmills are finding an even harder time to sell the lumber. The stave log market in southern Indiana is keeping sales with good white oak in them selling strong.

• The timber market is very strong at the present time. Landowners who have been holding off on selling trees should give serious thought to getting some Professional advice during this high price market.

• Timber price have remained very strong for the last 3 years.

• Mills are optimistic about the next year, most anticipate good prices to remain.

• Higher quality sales with larger timber continue to draw more interest as usual.

• Better access and terms continue to result in higher stumpage prices.

GENERAL MANAGEMENT COMMENTS:

• First, manage your woodland - have a plan, know what you have, and what you need to do, timber is valuable, and taxes are low; second, grow quality; third, if you want the best price and want to leave timber for the future, then hire a consulting forester; and fourth, don’t blacktop the access road and expect to get your timber out of the log yard to the county road.

• Access and terms are very important when selling timber.

• Invasive plants (bush honeysuckle, ailanthus) continue to spread. Too many stands are being cut without pre-harvest control (poor planning) and the stand is overrun within a year or two of the harvest, negatively impacting the long term health and productivity of the woods. Invasive species need to be controlled prior to any harvesting. Cost share assistance may be available to control the invasive plants thru the local Natural Resource Conservation Service office.

• Seeing a lot more high graded woods with young walnuts cut prematurely.

• Seeing too many diameter limit harvests with trees cut too early. Tree size is not a reason to harvest the tree and trees mature at different sizes on different sites.

• Woodland clearing (converting to cropland) is slowing down with the decline in crop prices but still happening way too often, especially on marginal soils.

Consulting Foresters that have contributed to this report in alphabetically order include: Arbor Terra Consulting (Mike Warner), Crowe Forest Management LLC (Tom Crowe and Jacob Hougham), Christopher Egolf, Gandy Timber Management (Brian Gandy), Glen Summers, Gregg Forestry Services (Mike Gregg), Habitat Solutions LLC (Dan McGuckin), Haney Forestry, LLC (Stu Haney), Multi-Resource Management, Inc. (Thom Kinney and Doug Brown), Meisberger Woodland Management (Dan Meisberger), Pyle Timber Sales and Management (David Pyle), Quality Forest Management, Inc (Justin Herbaugh), Ratts Forestry (Chuck Ratts), Schuerman Forestry and Bear Forestry (Joe Schuerman and Abe Bear), Stambaugh Forestry (John Stambaugh), Steinkraus Forest Management, LLC (Jeff Steinkraus), Turner Forestry, Inc. (Stewart Turner), and Wakeland Forestry Consultants, Inc. (Bruce Wakeland, Mike Denman, Andrew Suseland).